How acquirers quietly destroy what they just bought

Our 3 Key Take-away's

Capability acquisitions fail because of the acquirer's operating model, not poor execution. Most acquirers apply their scale-deal playbook to capability deals, systematically overwriting the value they paid for. Failure rates sit between 70 and 90 percent

Value destruction follows a predictable five-phase pattern, and the clock starts on Day 1. Each phase appears rational in isolation but collectively dismantles what made the target distinctive. 33 percent of acquired employees leave within the first year, with the highest performers leaving first

The central governance question must shift from "Are we on track?" to "Are we still aligned to the rationale?" This means operationalizing the deal rationale within 30 days, assessing technology decisions for irreversibility before they are made, and governing talent retention at steering level

1 Capability acquisitions are now one in five large deals, and the old playbook doesn't fit

A new class of deal now dominates corporate M&A. Industry estimates suggest that capability-driven acquisitions now represent roughly 20 percent of all large deals globally. These are transactions made to buy a distinctive capability rather than to scale an existing business[1]. The economic logic is straightforward: certain capabilities are faster to acquire than to build. However, the integration logic is anything but straightforward. A capability is not a balance sheet line. It is a working system of decision rights, operating model, technology stack, client relationships, and the people who run them. That system, not the asset, is what was bought. Yet most acquirers integrate capability deals using the same playbook designed for scale deals, a playbook built to harmonize, consolidate, and standardize. The mismatch is the entire problem.

The numbers are sobering. M&A failure rates, measured against the acquirer's own deal thesis, sit between 70 and 90 percent[2]. A separate analysis of S&P 500 transactions tracks a different but related signal: 46 percent of all deals are ultimately unwound, with the average time from acquisition to divestiture spanning a full decade[3]. The conventional explanations describe symptoms, not causes. Culture clashes, communication breakdowns, and under-resourced integration offices are real phenomena, but they sit on top of something deeper. The actual mechanism is structural. The acquirer's operating model behaves like an organizational gravity field: its reporting structures, approval workflows, technology architecture, decision rights, and institutional reflexes pull every part of the business toward the acquirer's defaults. It does not reject the target's distinctiveness deliberately or visibly; it does so by default, through the quiet weight of every standard process applied to a non-standard asset. This article names that mechanism, traces how it erodes value, and sets out the governance architecture required to prevent it.

2 The strategic rationale doesn't survive the handover

Consider the pattern that repeats across capability deals. A large organization acquires a smaller, specialized firm precisely because it operates differently. Faster decision cycles, deeper domain expertise, a distinctive client model the acquirer cannot replicate internally. The deal closes. Integration begins. The acquirer's teams follow their estab-lished playbook: corporate reporting structures are imposed, enterprise platforms are migrated, roles and processes are harmonized. Each step follows procedure. None is designed to protect what made the target valuable. Within two years, the differentiated capability has ceased to exist. Technically the integration succeeded. Strategically it failed. The handover is where this begins. The people who designed the deal rationale are almost never the people responsible for executing the integration. What gets handed over is legal scaffolding: share purchase agreements, transition service arrangements, regulatory filings. What does not get handed over is the translation of that rationale into operational terms: a decision framework specifying not just why the asset was bought, but which capabilities must be structurally protected and where the acquirer's defaults must not apply. The strategic intent may be clear at signing, but academic work on M&A integration finds that integration decisions translate into acquisition performance only through intermediate goals: without an explicit chain from rationale to operational milestones to performance, the link between plan and result breaks[4].

Execution teams fill this vacuum with precedent. The best playbooks include deal pur-pose, sponsors, and milestones. But a playbook designed for scale deals becomes counterproductive when applied to a capability acquisition. Research across 1,452 acquisitions[5] shows that the optimal integration depth depends on the type of synergy targeted: applying scale-deal integration depth to a capability deal mismatches the re-source reconfiguration the target requires. The mechanism is institutional: the playbook provides cover, because following the approved process is never questioned, even when the process is structurally wrong for the deal at hand. The result is a disconnect between the executive vision for what was bought and the operational reality of what is being built, invisible at the steering committee level because every milestone is techni-cally being met. When the playbook becomes doctrine, teams stop thinking from the deal logic and start thinking from the template.

3 Five phases turn the operating model into a value-destruction engine

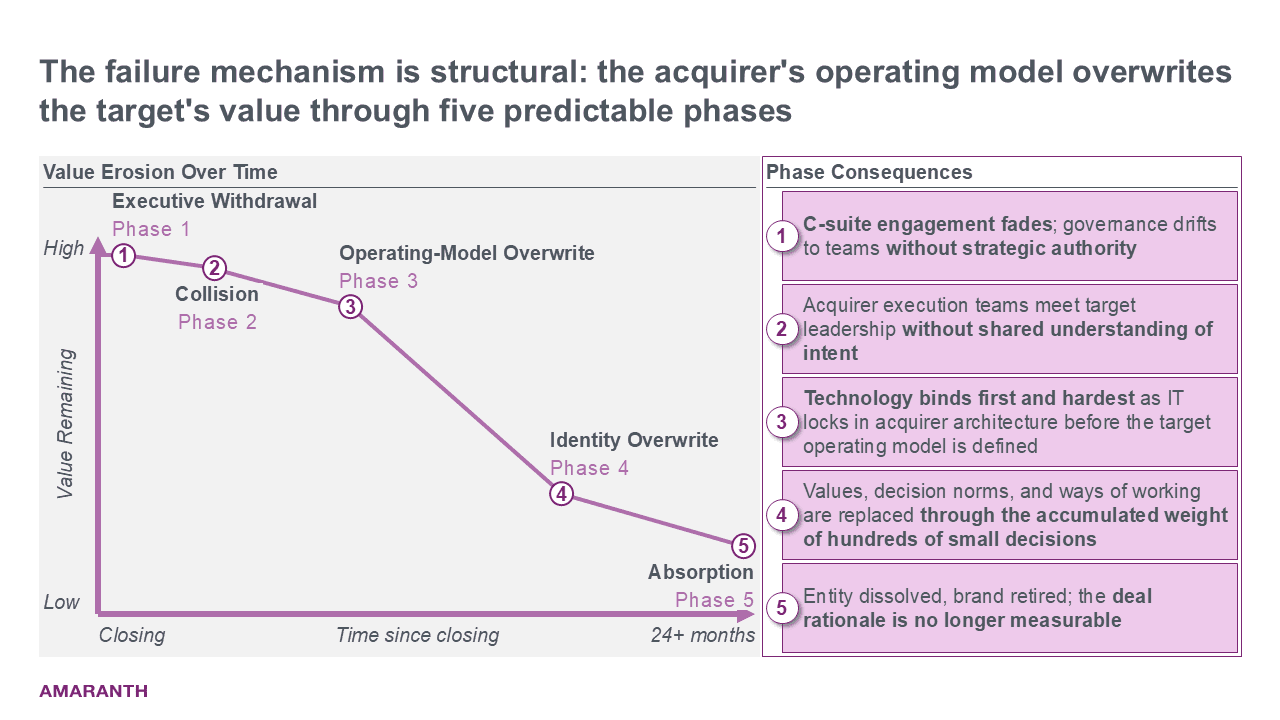

The erosion often follows a consistent five-phase sequence (Figure 1). Each phase appears rational in isolation. The destructive logic is visible only in aggregate.

Figure 1: Five Phases of Silent Value Destruction

Phase 1. Executive withdrawal. C-suite involvement is visible in the first weeks but competing priorities reassert themselves quickly. Integration governance drifts downward to teams that hold operational responsibility without strategic authority. The decisions that determine whether value is preserved are now made by people who were never in the room when the rationale was constructed.

Phase 2. Collision. The acquirer's execution teams and the target's leadership interact without a shared understanding of intent. Visions diverge, decision cycles slow, and neither side has the mandate to resolve fundamental disagreements about what the combined entity should become.

Phase 3. Operating-model overwrite. The acquirer's operating model fills the vacuum, and technology is where it hits first and hardest. IT enforces system migrations and platform consolidations onto the acquirer's enterprise architecture, before the target operating model has even been defined. These decisions are frequently treated as technical housekeeping, yet they are among the most consequential and least reversible choices in any integration. They are also among the most expensive: EY-Parthenon's analysis of 229 transactions[6] puts total integration costs between one and four percent of deal value, with technology costs ranking alongside severance and real estate as the most frequent one-time cost drivers. Finance then imposes standardized controls and reporting. HR harmonizes roles and compensation bands. Risk and compliance tighten processes. Middle management pushes for uniformity because uniformity is easier to govern. Each move feels rational locally. Collectively, they dismantle the operational foundations that made the target distinctive.

Phase 4. Identity overwrite. The target's culture and identity are progressively replaced by the acquirer's: values, decision norms, ways of working. The people who built the target no longer recognize the organization they work in. The original identity is erased not through a single decision, but through the accumulated weight of hundreds of small ones.

Figure 2: Four Waves of Talent Erosion

Talent erosion runs underneath the five phases (Figure 2). It mirrors the integration timeline but lags behind it. In the early months, people watch and wait. Effort and initiative drop, but few leave immediately. As misalignment becomes visible and direction stays unclear, the best people begin exploring external options. Then the departures begin in waves. The most talented and most mobile people leave first. They see the problems earliest and have the strongest options outside. Each departure takes knowledge and relationships with it. The magnitude is well documented: U.S. Census data covering 230,000 acquired employees shows 33 percent leave within the first year, 2.75 times the rate of comparable hires, with the effect most pronounced among high earners[7]. A second wave follows twelve to twenty-four months later, triggered by the belated imposition of the acquirer's target operating model. That model was designed for the acquirer's legacy business, not the acquired vertical. By then, the remaining talent pool has been adversely selected: those who stay are disproportionately those who have not found alternatives or whose contractual terms discourage departure. People optimize for personal stability, not creation.

Phase 5. Absorption. The entity is absorbed: legal structure dissolved, brand retired, remaining staff folded into the acquirer's existing structures. Nobody can point to the value the deal was supposed to create. The integration is declared complete. The deal rationale is no longer measurable in any operational metric.

4 Three political forces keep the mechanism invisible to steering

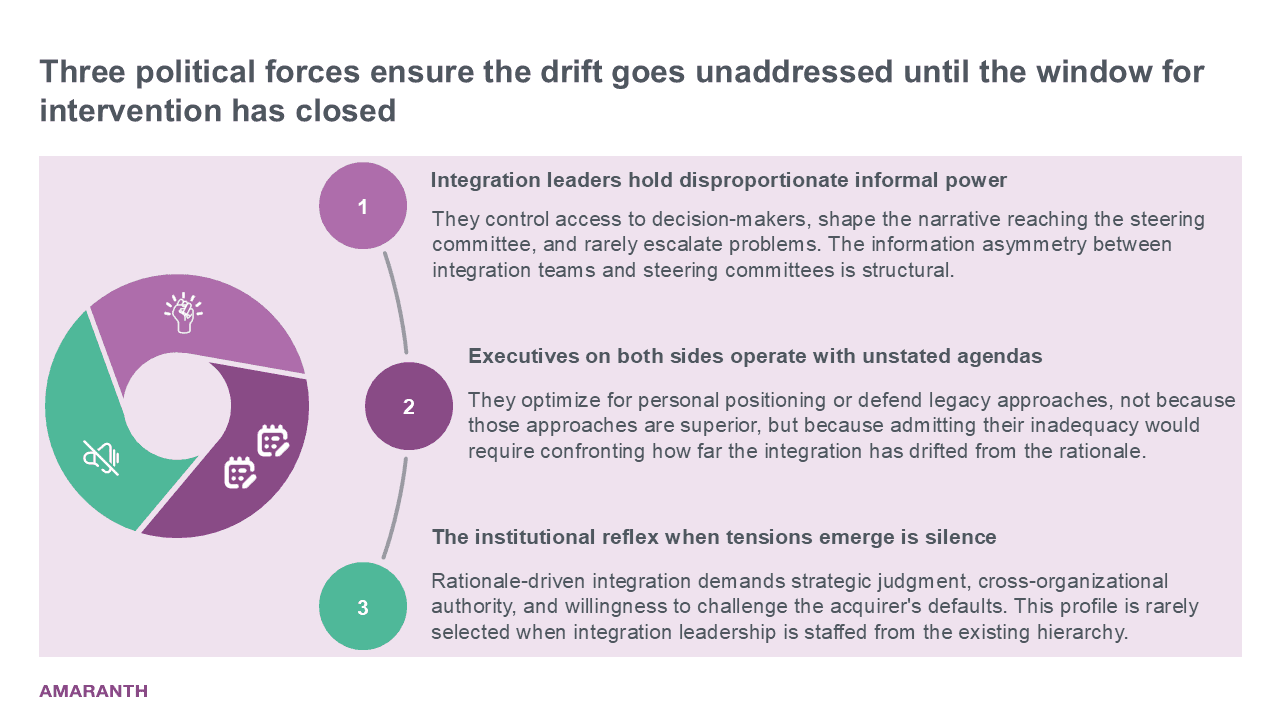

Every failed integration has a political anatomy visible to everyone and acknowledged by no one. Three forces (Figure 3) consistently shape it.

Figure 3: The Three Political Forces

First, integration leaders inside the acquiring organization hold disproportionate informal power. They control access to decision-makers, shape the narrative that reaches the steering committee, and rarely escalate problems because escalation signals weakness.

Second, executives on both sides operate with unstated agendas. They optimize for personal positioning or defend legacy approaches not because the approaches are superior, but because admitting their inadequacy would require confronting how far the integration has drifted.

Third, the institutional reflex when tensions emerge is silence. The uncomfortable truth is not that integration leaders lack talent. It is that the structural demands of a rationale-driven integration exceed what the standard assignment process is designed to match. The role requires strategic judgment, cross-organizational authority, and the willingness to challenge the acquirer's defaults, a profile rarely prioritized when integration leadership is staffed from the existing hierarchy. Steering committees continue to review milestone trackers while the actual determinants of success play out in corridors. Leaders absorb the consequences rather than confront the structural reasons value was destroyed, because doing so would mean admitting the governance architecture was never designed to prevent it. That gap is what rationale-anchored governance is built to close.

5 Replace milestone tracking with rationale-anchored governance

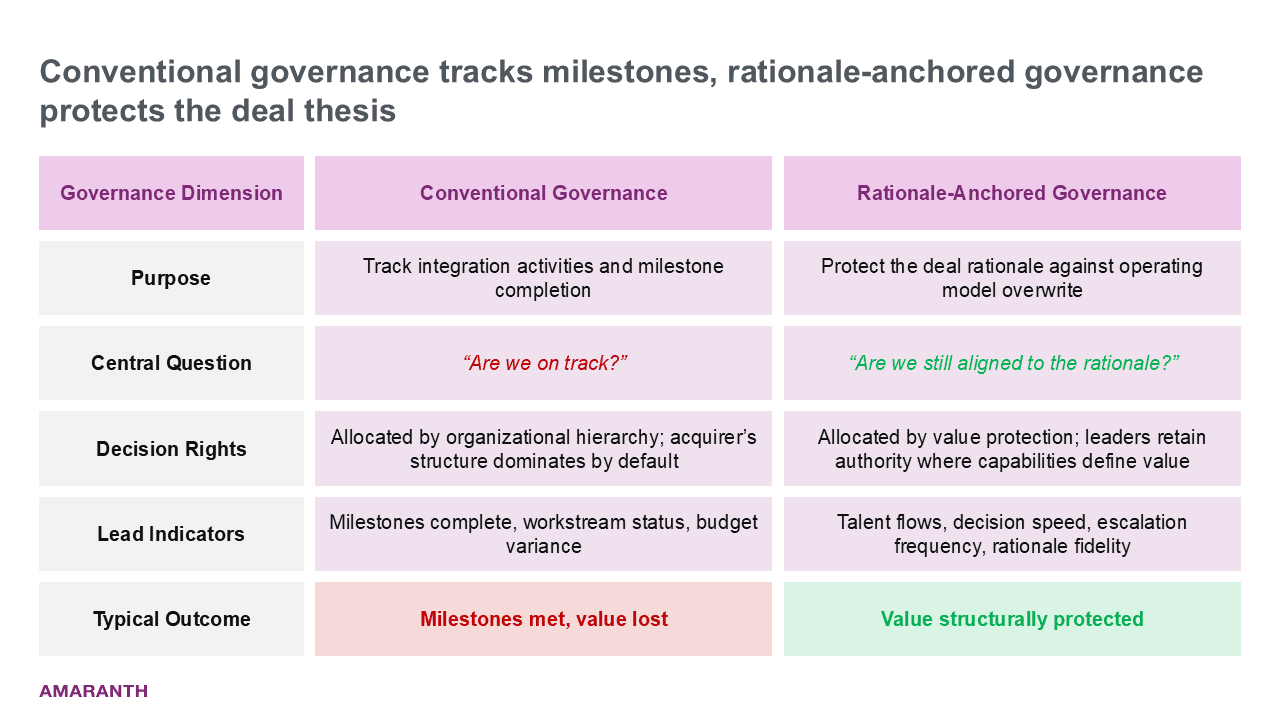

The conventional response is an Integration Management Office with workstream leads, status reports, and weekly cadences. It tracks activities. It does not protect value. What is required is rationale-anchored governance: a structure that ties every integration decision back to the deal rationale and tests technology, organizational, and commercial choices against it before they become irreversible (Figure 4).

Figure 4: Conventional vs. Rationale-Anchored Governance

First, translate the deal rationale into an operational decision framework before or immediately after closing. The framework specifies what was bought, which capabilities define the value, and where the acquirer's standardization is permitted versus where it endangers the value thesis. This applies with particular force to technology decisions: platform migrations, architecture consolidations, and system decommissioning must be governed by the rationale, not by the acquirer's IT roadmap.

Second, allocate decision rights based on value protection, not organizational hierarchy. Leaders within the acquired business who carry rationale-relevant capabilities need real authority for a defined period. Support functions need explicit guardrails on where harmonization is appropriate and where it must wait. C-suite commitment must be structural, not ceremonial.

Third, expand governance forums beyond progress reporting to include drift detection. Traditional milestones and financial KPIs remain necessary, but they are lagging indicators. The central question at every steering meeting is not “Are we on track?” but “Are we still aligned to the rationale?” Talent flows, decision speed, and escalation frequency are additive leading indicators. They signal whether the rationale is still intact long before financial metrics register the damage, and they complement rather than replace traditional progress and financial reporting.

Change management in this model is not an ancillary workstream. It is the mechanism through which the integration's strategic intent is defended against institutional inertia. Communication cannot compensate for missing governance. But governance without sustained communication into both organizations will be undermined by the default behaviors it was built to override.

These conditions are necessary but not sufficient. The organizations that consistently protect deal value go further: they establish an independent integration authority with the seniority and mandate to challenge the acquirer's defaults. This authority is not an advisory function. It is a structural counterweight to operating-model gravity. They staff the integration with practitioners who have seen the mechanism from both sides of the transaction and understand where the irreversible decisions are made.

And critically, they treat talent retention as a steering-committee responsibility, not an HR workstream. Identifying capability-carriers by name, documenting their role in the value thesis, and giving them reasons to stay that are not just financial is the difference between buying a capability and buying the shell that used to contain one.

The window for these interventions is narrow. Technology architecture decisions create path dependencies from the moment they are implemented. Platform migrations, system decommissioning, and data consolidation are the decisions that bind. Research confirms that IS decisions partially mediate the effects of all other integration variables on outcomes. Once systems are decommissioned, the technical foundation for the acquired business model no longer exists independently[8]. By the time a steering committee recognizes the drift, the systems have been migrated, the people who embodied the capability have left, and authority has been reassigned to the acquirer's defaults. None of these are recoverable on the timelines an integration runs. The question, therefore, is not whether to act when drift becomes visible. It is whether the governance architecture is in place before the window closes.

The artifact that ties these conditions together is the Investment Hypothesis. It translates the deal rationale into measurable terms across three dimensions, People, Process, and Technology, with explicit KPIs that track value secured against the deal thesis, not activity completed:

People: retention of named capability-carriers in their rationale-relevant roles, and their productivity against pre-deal baseline.

Process: decision velocity on rationale-relevant matters, and revenue retained from clients and products named in the deal thesis.

Technology: availability of the platforms that deliver the capability to customers, and synergy realization booked against the deal model.

Each dimension is paired with an assessment framework that tests it at every gate, and a named sponsor who owns the safeguard when reality diverges from thesis. This is what the steering committee tracks: the value drivers of the deal, not the milestone playbook. The shift is from asking “are we executing the plan?” to asking “is the plan still the right plan?”

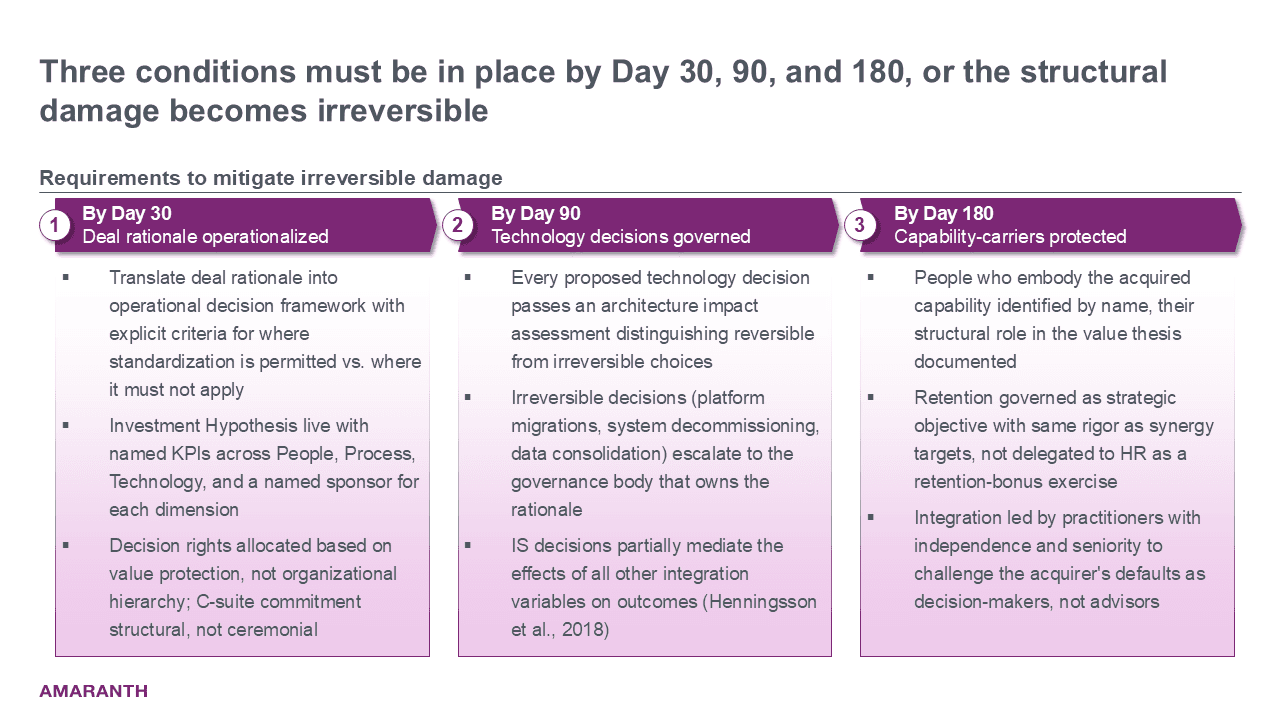

The implications are operational and immediate, and they sequence on a tight clock (Figure 5).

Figure 5: The 30/90/180 Day Framework

By Day 30: the deal rationale must exist as an operational decision framework, not a strategy deck. The framework states explicit criteria for where the acquirer's standardization is permitted and where it must not apply. The Investment Hypothesis must be live by the same date, with named KPIs and a named sponsor.

By Day 90: every proposed technology decision must pass an architecture impact assessment that distinguishes reversible from irreversible choices. Irreversible decisions escalate to the governance body that owns the rationale.

By Day 180: the people who embody the acquired capability must be identified by name, their structural role in the value thesis documented, and their retention governed as a strategic objective with the same rigor as synergy targets. The integration itself must be led by practitioners with the independence and seniority to challenge the acquirer's defaults, not as advisors but as decision-makers with the mandate to override standard process where the rationale demands it.

These are not refinements to the standard playbook. They are a fundamentally different governance architecture. Most organizations do not possess it internally. They must build or acquire it before the window closes.

If governance does not structurally protect the deal rationale from the beginning, the acquirer's operating model will quietly destroy the value it just bought. Not through failure. Through default.

Sources:

[1] Bain & Company (2020). Integration: Why less is more in capability deals. Bain Global M&A Report 2020.

[2] Christensen, C. M., Alton, R., Rising, C., & Waldeck, A. (2011). The new M&A playbook. Harvard Business Review, 89(3), 48–57.

[3] MIT Sloan Management Review (2025). Why mergers fail and how to spot trouble early. MIT Sloan Management Review.

[4] Cording, M., Christmann, P., & King, D. R. (2008). Reducing causal ambiguity in acquisition integration: Intermediate goals as mediators of integration decisions and acquisition performance. Academy of Management Journal, 51(4), 744–767.

[5] Chaturvedi, T., & Weigelt, C. (2024). Operating synergy and post-acquisition integration in corporate acquisitions: A resource reconfiguration perspective. Long Range Planning, 57(3), 102–428.

[6] EY-Parthenon (2025). Beyond the deal: Accurately estimating M&A integration cost. EY Insights: Strategy and Transactions.

[7] Kim, J. D. (2024). The challenge of retaining startup talent after an acquisition. Harvard Business Review, February 2024.

[8] Henningsson, S., Yetton, P. W., & Wynne, P. J. (2018). A review of information system integration in mergers and acquisitions. Journal of Information Technology, 33(4), 255–303.

About the author(s)

Consultant

Pascal Fabry

3+ years of experience in transformation and strategic advisory across the automotive, financial services, and healthcare sectors. Special focus on platform strategy and organizational transformation. Former professional work at CORE SE and Globus Markthallen.

Executive Advisor

Mauritz von Lenthe

Industrial Engineer with 5+ years of expertise in strategic consulting, data science, and enterprise architecture. Special focus on digital platform strategy, compliance and data/AI. Former professional work at CORE SE, Digital Spine, and BMW.